The increase in wind and solar energy brought down electricity prices in March, despite the low levels of hydropower in Latvia

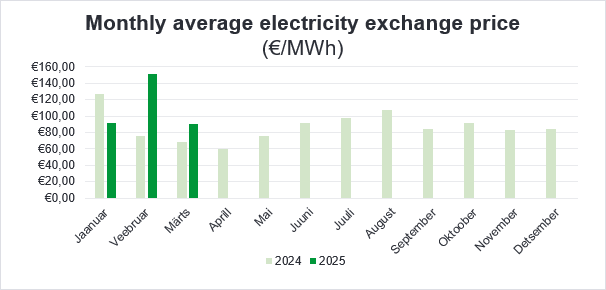

Compared to February, electricity prices in March were approximately 41% lower, at a level of €90.2 per megawatt-hour. The price decrease was supported by nearly twice as much wind power generation across the Baltics, reduced heating demand and the addition of solar energy.

Compared to March 2024, the price of electricity this year was 32% higher. The price remained higher due to the lack of transmission capacity across the entire Baltic region and nearly 50% lower hydropower production in Latvia.

Decreased hydropower production in Latvia and increased solar and wind production in the Baltics are putting the market in a new situation

In March, an exceptional anomaly emerged at times on the Baltic markets: wind and solar production is at the highest level in history (718 gigawatt-hours of electricity were produced across the Baltics in March), but hydropower production coming from Latvia is at a record low in the context of the past three years. While in March last year nearly 695 gigawatt-hours of electricity were generated from hydropower in Latvia, this year production during the same period amounted to approximately 271 gigawatt-hours – nearly 61% less. Compared to March last year, we consumed nearly a quarter more wind and solar energy across the Baltics, and nearly a third more energy based on fossil fuels. We consumed approximately 60% less hydropower, primarily sourced from Latvia and, to a lesser extent, from Lithuania.

Volatility in the Baltic price areas is here to (temporarily) stay

The previously mentioned market anomaly and the limited transmission capacity between countries largely explain the highly volatile state of our electricity market. Renewable energy, which is difficult to forecast but cost-effective for consumers, and electricity generated from dispatchable capacities and fossil fuels have become the main price setters on the market. Due to the limited availability of energy imports from the Nordics, we are increasingly seeing days when prices are low during the daytime, but during the morning and evening peak demand hours, more expensive power plants are activated, potentially driving prices up to ten times higher than the average. So far, the market has shown that price volatility on the Baltic electricity exchanges will not decrease before large-scale battery storage is added to the market.

In the coming months, solar generation is expected to be added to production, significantly lowering daytime prices, while the absence of Estlink 2 will significantly raise evening prices

With the arrival of April, the growing solar energy production is starting to play a greater role across the Baltics. This significantly lowers prices during the daytime, but brings greater price fluctuations in the evening when more expensive power plants are activated. Due to the low capacity of electricity imports and the significantly lower production of hydropower in Latvia, we can also expect days in April when the price remains low during the day, but in the mornings and evenings the exchange price increases several times compared to the midday prices.

The closer we get to summer, the more we feel the effect described above: renewable energy is not sufficient to meet demand during the evening hours, when solar generation disappears. In addition, it is not possible to import electricity from Finland in the same volumes as before, which leads to a significant rise in prices during the evening hours.

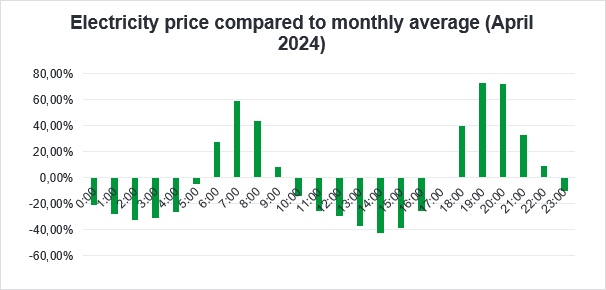

April last year suggests cheaper hours during the night and around midday

To assess the impact of additional solar production, we can compare the average price of each hour with the monthly average price. Both April 2023 and April 2024 show the same pattern: in the morning hours between 06:00 and 08:00, electricity prices are approximately 60% higher than the monthly average, and in the evening hours between 18:00 and 20:00, nearly 70% higher. For example, if the monthly average price in April were €100 per megawatt-hour, the average electricity price between 18:00 and 20:00 would be €170 per megawatt-hour.

At the same time, prices during the hours from 00:00 to 04:00 throughout April have been up to 30% lower than the monthly average, and between 11:00 and 15:00 even 40% lower than the monthly average. Although the price behaviour of previous years is not a predictor of the future, it provides a clear indication of how it makes sense to manage electricity consumption in April.

Natural gas

Unlike the turbulent February, the gas market was calmer in March. Prices fell by more than 13% from the price peak of 3 March (€47 per megawatt-hour) to €40.9 per megawatt-hour by the end of March. In March, above-average temperatures in Europe played an important role in the gas market by reducing heating demand. Strong wind power production across Europe also reduced gas demand.

The price decline was also supported by easier access to LNG – according to various sources, 15% more LNG was imported in March than in February. Prices have continued to be influenced by geopolitical events: a possible ceasefire in the Russia–Ukraine war has sparked speculation among market participants about the recovery of natural gas reserves in Europe.

Carbon allowances

After a volatile February, March was relatively calm on the carbon allowance market – prices moved without major fluctuations and decreased by approximately 6% over the course of the month. In February, speculation about an increase in the number of carbon allowances led to a reduction in allowance prices, which fell by approximately a fifth from the early-February peak. The month of March was therefore calmer: the market incorporated the new situation into its business models, which in turn led to slight price fluctuations. By the end of March, the price of carbon allowances was €67 per tonne of carbon.

Karl Joosep Randveer, Energy Trading Analyst at Eesti Energia

The market overview has been compiled by Eesti Energia according to the best current knowledge. The information provided is based on public information. The market overview is presented as informative material and not as a promise, proposal or official forecast by Eesti Energia. Due to rapid changes in the regulation of the electricity market, the market overview or the information contained in it is not final and may not correspond to future situations. Eesti Energia is not liable for any costs or damages that may arise in connection with the use of the information provided.